Massive Institutional Gold Market Change

Posted 01 Sep 2009

There is a massive change in the institutional gold market. The CME Group has announced, "In response to market needs, CME Group will offer a clearing service for the OTC London gold forward market beginning September 20, 2009 for trade date September 21, 2009."

After an analysis of the governing terms, policies, procedures and methods I think this scheme will allow for gold demand to be shunted into gold substitute products and keep the price of gold in fiat currencies low while entangling the gold substitutes with increased risks.

Counter-party Risk

While similar there are differences between future and forward contracts. For example, future contracts are traded on exchanges, use margin and are marked to market daily. In contrast, forward contracts are generally privately traded over-the-counter (OTC derivatives) between two parties and are not marked to market.

Therefore, forward contracts are subject to greater counter-party risk than future contracts. This may be a reason why there was nine weeks of silver backwardation in early 2009 with the LBMA forwards while not with the futures.

Based on the following new press release and the FAQs for Cleared OTC London Gold Fowards there are a few key features investors should be cognizant of and while I will not address all of them for brevity sake I will hone in on some of the most important.

Contracts remain as forwards in clearing and are not converted to futures contracts. Every trade establishes a new open position. There is no liquidation. Upon reaching delivery, positions are netted down and CME Clearing remains in the delivery process.

Delivery occurs at London Precious Metals Clearing (LPMCL) member banks using "London Good Delivery Gold. ... Clearing coverage for all good forward maturities that are physically deliverable into unallocated "London Good Delivery" gold extends 10 years out. [emphasis added]

This is interesting given the standard industry practice to 'net' purchases and sales. The London Precious Metal Clearing Limited states:

The bullion market has generally advocated the netting of same day value trades by counterparty, as a means to reduce the number of settlements, but also and more importantly, in order to reduce the amount of credit risk both while the trades are live but not yet due for settlement, as well as at the actual point of settlement.

Note: Netting is particularly important given that the vast majority of bullion trades are against US dollars, when the metal leg is settled in London by 4.00pm, but party due to receive the dollar counter-value in New York will not normally know whether or not the dollars have been received in their account, until the US dollar clearing closes at the end of the New York business day.

Why would the CME want to provide for no liquidation and wait until delivery to net down positions and thus increase the amount of counter-party and credit risk in the transactions?

Guarantee

Question 22 asks:

How are the contracts guaranteed?

CME Clearing provides two forms of guarantee: a counterparty guarantee and a delivery guarantee.

When OTC forward trades are substituted in the clearing system, CME Clearing becomes the counterparty to every buyer and seller. Once these trades are accepted for clearing, the counterparties look to CME Clearing for financial performance during the life of the transaction.

The second guarantee occurs at settlement. With Cleared OTC London Gold Fowards, the clearing house remains in the delivery chain and provides each party the full comfort that the clearing house will effectively make delivery of dollars and gold.

These two guarantees add convenience for the parties involved and is a primary reason for exchanges. But the failure of an exchange, like the COMEX failing to deliver, is possible and almost happened with Deutsche Bank according to securities attorney Avery Goodman. Those parties availing themselves of acquiring bullion through these cleared forwards should take adequate precautions to minimize their risk and I will mention these later.

Delivery

Question 23 asks:

How will delivery be made?

For delivery, all participants will establish an unallocated gold bullion account at a London Precious Metal Clearing Ltd. bank. Standing settlement instructions will need to be provided to CME Clearing for each clearing position account. CME Clearing will become counterparty in the delivery process by opening accounts at LPMCL banks to facilitate this process. CME Clearing will not become a clearing bank itself or manage vault facilities which hold precious metals in storage.

What Is the LPMCL?

In April 2001 the six LBMA members that offer clearing services formed a not-for-profit company called London Precious Metal Clearing Limited.

These six members include Barclays Bank PLC, The Bank of Nova Scotia-ScotiaMocatta, Deutsche Bank AG - London Branch, HSBC Bank USA National Association - London Branch, JPMorgan Chase Bank and UBS AG.

The LPMCL website is, inconveniently, in javascript which keeps the text out of major search engines like Google and makes it difficult to provide hyperlinks to the relevant citations.

Under the Introduction in the Physical section clear at the bottom they assert that "Unallocated accounts do not entail specific bars being set aside and the customer has a general entitlement to fungible metal. Unallocated accounts are the most convenient and commonly used method of holding gold and silver. The owner is an unsecured creditor of the clearing member."

Under the LPMCL Unallocated User Agreement an

'Unallocated Account' means, in relation to a Precious Metal, the account(s) maintained by us in your name recording the amount of that Precious Metal which we have a contractual obligation to transfer to you (or, in the case of a negative balance, if so permitted by us, which you have a contractual obligation to transfer to us).

An unallocated gold account does not have the same risk profile as physical gold bullion held either personally or through a trusted third party vaulting service like GoldMoney in bailment. An unsecured debtor is extremely different from an absconding bailee.

Governing Rules

Question 13 asks:

What Exchange rules will govern this service?

All disputes are governed by the COMEX and CME rules and regulations. Once the trade is substituted into clearing, any prior legal agreements will fall away and both parties will come under the rules and regulations of the COMEX and CME.

This is particularly interesting that there would be a merger and integration clause to supplant prior contracts with COMEX rules.

CFTC Sanction

Under a 22 February 2005 notice from Nancy Minett, Vice President of the Compliance Department at the Commodities Futures Trading Commission, provides that:

The New York Mercantile Exchange, Inc. ("NYMEX" or the "Exchange") hereby notifies the Commodity Futures Trading Commission ("CFTC") that, as set forth in the attached rule interpretation, it will accept gold-backed ETF shares as the physical commodity component for EFP transactions involving COMEX gold futures contracts

GLD ETF Problems

Why the CFTC would allow supposedly gold-backed ETF shares to satisfy the physical commodity component in an exchange of futures for physical transaction baffles me. In December I wrote A Problem With The GLD ETF which reads:

See "Risk Factors" starting on page 6." Page 11 states "Neither the Trustee nor the Custodian independently confirms the fineness of the gold allocated to the Trust in connection wtih the creation of a Basket [issuances]." Page 12 "In issuing Baskets, the Trustee relies on certain information received from the Custodian which is subject to confirmation after the Trustee has relied on the information.

If such information turns out to be incorrect, Baskets may be issued in exchange for an amount of gold which is more or less than the amount of gold which is required to be deposited with the Trust." There is no assurance that the 'gold' held in the ETFs is actually the same gold as defined under the periodic table.

I then followed up that article with Another Problem With The GLD ETF which reveals,

The latest 10-K (Commission File Number 000-32356) on pages 26 and 18 respectively: " Gold held by the Custodian's currently selected subcustodians and by subcustodians of subcustodians may be held in vaults located in England or in other locations." and "In addition, the Trustee has no right to visit the premises of any subcustodian for the purposes of examining the Trust's gold or any records maintained by the subcustodian, and no subcustodian is obligated to cooperate in any review the Trustee may wish to conduct of the facilities, procedures, records or creditworthiness of such subcustodian."

Not only does the GLD ETF not have to store physical gold bullion as defined under the periodic table but any gold it may hold the Trustee has no right to examine even for the purpose of an audit of the physical gold bullion. Anyone who is willing to accept supposedly gold-backed ETF shares instead of physical gold as defined under the periodic table may be brain dead.

Greenlight Capital Flees GLD

For example, in a 13 July 2009 letter to investors David Einhorn of Greenlight Capital, a multi-billion dollar hedge fund with the largest holding in GLD, wrote:

{kind=link}

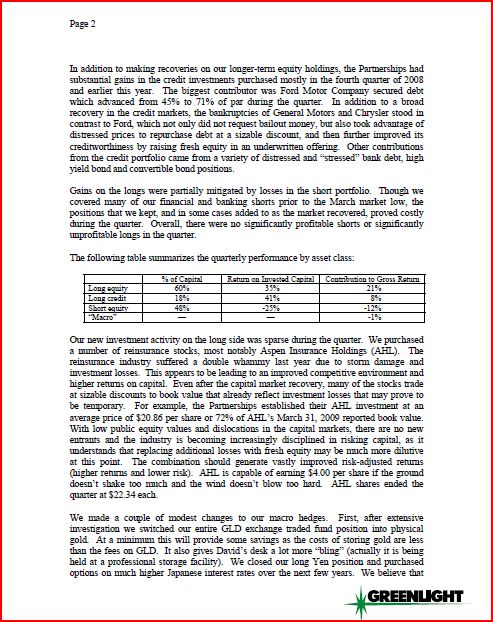

We made a couple of modest changes to our macro hedges. First, after extensive investigation we switched our entire GLD exchange traded fund position into physical gold. At a minimum this will provide some savings as the costs of storing gold are less than the fees on GLD. It also gives David's desk a lot more "bling" (actually it is being held at a professional storage facility) [emphasis added].

In addition to needing to send David a bill for my articles about the GLD ETF it also makes me wonder whether the CFTC is in denial or complicit?

Physical Gold Is Getting Scarce

This further consolidation of the gold price determinant via the OTC forwards with the COMEX will make the central bank gold price suppression scheme easier to manage because gold demand that was previously satisfied with physical bullion through forward contracts between private parties can now be satisfied with unallocated gold accounts or, in other words, paper substitutes for physical bullion.

But the increased convenience and lower transaction costs come with the latent cost of increased counter-party risk which may later prove lethal to one's financial condition.

And as Norman R. Nelson, Executive Vice President and General Counsel of The Clearing House Association LLC declared on behalf of the Federal Reserve in Bloomberg v. Federal Reserve, the revelation of such trade secrets would be "information virtually everyone would consider potentially disastrous."

I hypothesize that the reason for this move is that physical gold bullion is getting increasingly scarce. After all, annual worldwide production is only about 70 million ounces or $65B compared to the quantitative easing by the Federal Reserve, Bank of England, etc.

Gold is cash and the risk-free asset because at all times and in all circumstances gold and silver are money and also essential checks and balances in the political machinery.

While the fiat currencies represent the common stock of nations and their evaporation of the FRN$ portends difficult circumstances. Now is the time to start implementing provident living principles, preparing for survivalism in the suburbs and learning how to protect your personal and financial privacy.

Conclusion

The green shoots are but illusions because the administration is intentionally exacerbating the greater depression. There is another market crash coming. Currency controls are being heightened.

Do not mistake this brief reprieve and added ammunition for the gold cartel as a recovery. Attempting to suppress interest rates by manipulating the gold price through paper instruments, like settling either COMEX futures contracts or OTC forwards with GLD ETF shares, is a policy destined for failure and is 'potentially disastrous' on a massive scale.

I titled my book The Great Credit Contraction and it has only begun. Like David Einhorn's example shows capital is moving into the safest and most liquid assets with physical gold bullion, either a coin in your hand or stored with a trusted professional storage facility like GoldMoney and not the GLD ETF or COMEX futures contract, is the safest and most liquid of them all.

Disclosure: Long physical gold, silver and platinum with no position in GLD or SLV.